By Lambert Guilbault, Manon Esperandieu, Catherine Athenes, Ana Mingo, Jonathan Vanherberghen, and Ute Just

The EU’s Carbon Border Adjustment Mechanism (CBAM) is supposed to equalise carbon costs between domestic production and imports. In its current form, however, it falls short for aluminium. By excluding recycled post-consumer scrap as a precursor in imported products (as proposed in the European Commission’s recent review), CBAM and the EU ETS create a structural asymmetry on carbon costs between domestic and imported products. This distorts competition, weakens the EU’s recycling base and will damage raw materials’ circularity in Europe at a time when we need it the most.

As the European Parliament and member states take forward the Commission’s December 2025 review of CBAM, the window to correct this design flaw before it becomes entrenched into CBAM, is narrowing.

The scrap loophole is not difficult to fix. It is, rather, a question of political will: treating all recycled aluminium scrap, whether pre- or post-consumer, as a precursor within CBAM’s scope and assigning it the same carbon cost as primary aluminium would level the playing field on carbon costs, limit circumvention, and enable CBAM to fulfill its objective.

At stake is not a technical detail. It goes to the heart of the credibility of CBAM, one of the EU’s most consequential climate policies, and more broadly, to Europe’s approach to protecting its critical raw materials, the resilience of its domestic low-carbon industrial base, its strategic autonomy, and the credibility of its circular economy ambitions.

Aluminium: a strategic material Europe can ill afford to lose

Aluminium is deemed critical by both the EU and NATO, and with reason. It underpins everything from power grids and transport to defence and clean energy.

As a globally traded and energy-intensive commodity, it is also highly exposed to carbon leakage. Over the past two decades, higher energy prices, rising carbon costs and weaker investment conditions in Europe have contributed to the loss of around two-thirds of its primary production capacity, much of it shifting to more carbon-intensive regions. It has left Europe increasingly import-dependent on aluminium. The risk of this import dependence is now on full display as supplies from the Persian Gulf are disrupted and threaten to cause real shortages in the EU market.

This matters also from a climate perspective, because European aluminium is over 50% less carbon-intensive than the global average. Production capacity has not disappeared when European production has been curtailed; it has shifted, often to higher-emission regions.

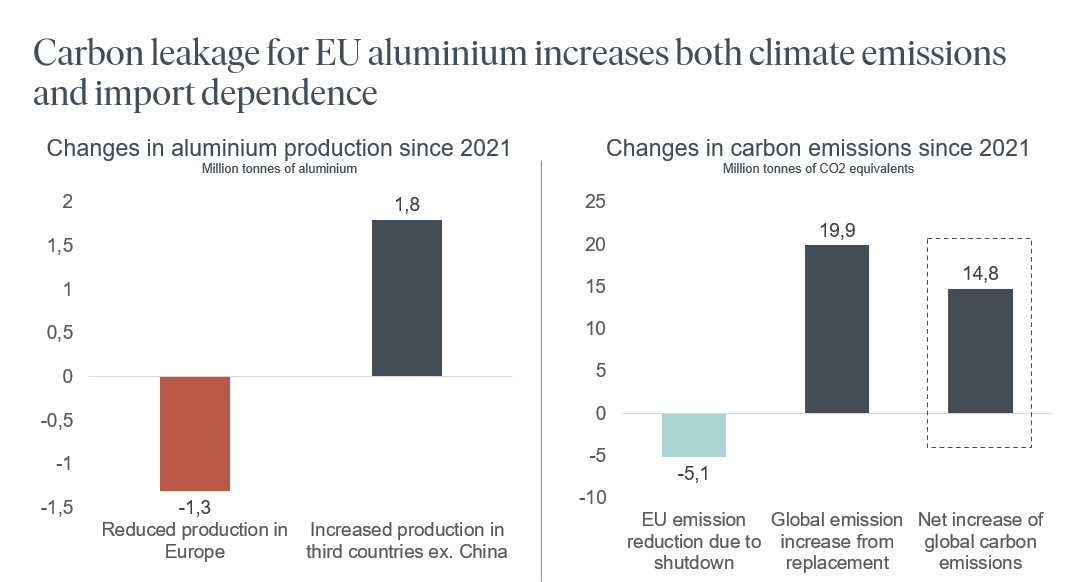

EU/EEA aluminium production cuts since 2021 reduced emissions domestically (-5.1 Mt CO₂) but increased global emissions (+14.8 Mt CO₂) due to higher-carbon production abroad. Source: CRU; Hydro analysis.

Indeed, the pressure on the sector is already visible. Since 2021, Europe has lost around 1.3 million tonnes of aluminium production. That’s more than 50% of primary aluminium production capacity. At the same time, output in third countries has increased by roughly 1.8 million tonnes. The result has not been lower but higher emissions: an estimated increase of nearly 15 million tonnes of CO2 globally. Carbon leakage is no longer a future concern; it is already happening.

Excluding post-consumer scrap creates a clear pathway to avoid CBAM costs

The Commission has proposed to include secondary aluminium based on pre-consumer scrap in CBAM. This is a useful step, but incomplete. By excluding recycled post-consumer scrap, roughly 25% of global aluminium supply will avoid CBAM costs.

The issue is not theoretical. If recycled post-consumer scrap carries no carbon cost under CBAM, it becomes the preferred route for imports seeking to minimise carbon cost exposure.

It also creates a clear risk of circumvention, as non-EU producers may overstate or wrongly claim the use of post-consumer scrap.

In practice, this means that a very large share of aluminium products could enter the EU market without carbon costs equal to those in Europe.

European recyclers already pay a carbon price, but CBAM fails to recognise it

Once melted, all aluminium is identical and priced accordingly. Whether produced from primary metal, pre-consumer scrap, or post-consumer scrap, the final product is indistinguishable in quality and competes in the same market.

This is reflected in pricing: scrap prices follow primary aluminium prices. When primary prices rise, due to tariffs or carbon costs, scrap prices increase as well.

The implication is clear: carbon costs applied to primary aluminium under the EU ETS or CBAM are already indirectly reflected in scrap prices.

In the EU and EEA, primary aluminium is subject to EU ETS carbon costs, which are therefore embedded in scrap prices. In practice, all aluminium scrap, including post-consumer scrap, already contains an implicit carbon cost.

European recyclers thus face carbon costs in their inputs, even when using recycled material. This mirrors indirect carbon costs in electricity markets, where CO2 costs are passed through market prices.

By contrast, in most third countries, scrap prices do not systematically reflect carbon pricing. Imported recycled aluminium may therefore not carry comparable CO₂ costs and, unlike in the EU, the scrap content has never been subject to a CO2 cost in its lifecycle.

The result is a mismatch: European recyclers already pay a carbon price, just not one that CBAM recognises, while imports may not.

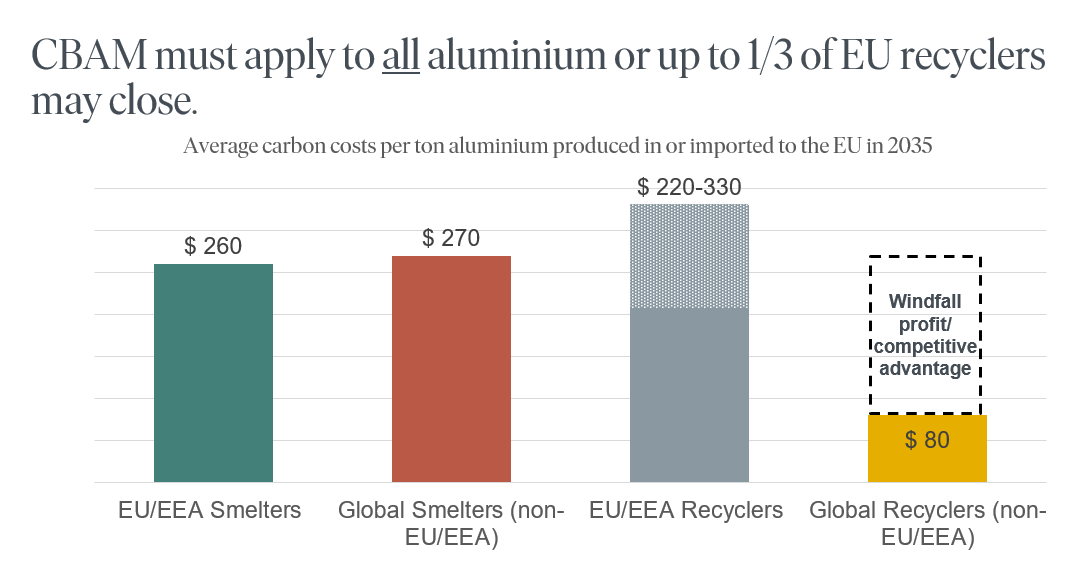

Under current CBAM design, global recyclers face significantly lower carbon costs (~$80/tonne) than EU producers (~$220–330/tonne), creating a competitive imbalance. The ETS price in 2035 assumed at€140/tonne. Recycler cost range estimate: EU/EEA Pre-consumer scrap price assumed to be EU primary price including CBAM market premium, which increases recycler costs. Low-cost recyclers assumed to obtain cheaper post-consumer scrap (75% PCS with a 30% CBAM impact and 25% std. ingot); Both assumed higher direct emissions cost. Source: Arkwright research; Hydro analysis.

By 2035, European recyclers could face carbon costs of $220-330 per tonne, reflecting both direct EU ETS costs and the pass-through of carbon costs in scrap. Non-European recyclers, by contrast, may face costs as low as $80 per tonne, as these buy aluminium scrap in local markets that do not have any carbon costs.

This gap is significant. It creates a large structural advantage for imports and a corresponding disadvantage for European recycling.

Excluding post-consumer scrap shifts the circular economy out of Europe

A circular economy cannot be built by weakening the industries that sustain it. The consequences of not including post-consumer scrap and thereby all aluminium scrap, extend beyond trade flows.

If recycled aluminium produced outside Europe can enter the EU market without equivalent carbon costs to European recyclers, the competitive pressure will lead to closures in Europe, reduced circularity and increased import dependence on a critical raw material used for energy production, defence, IT and transport.

Rather than strengthening the circular economy, it would shift recycling capacity abroad while weakening it within the EU. The result is not greater circularity, but less European recycling, greater dependence on imports, reduced European strategic autonomy, and increased exposure to higher-emission production elsewhere.

Estimates already suggest that up to a third of Europe’s aluminium recycling capacity could be at risk if the loophole persists.

Equal treatment of all scrap is needed for a level playing field. Failure to act would entrench a distortion at the heart of CBAM

If the goal is to ensure equal carbon costs for equal products, then all aluminium, regardless of whether it originates from primary metal, pre-consumer scrap, or post-consumer scrap, should be treated equally and consistently once it enters the EU market.

This requires bringing all secondary aluminium content within the scope of CBAM and assigning it the same carbon costs as primary aluminium.

These are targeted adjustments. They do not require reopening the regulation, only aligning it with its stated objective.

CBAM is still taking shape through the legislative process. How it treats aluminium scrap will be an early test of whether it can deliver on its central promise.

The European Parliament and member states have an opportunity to correct a design flaw before it becomes entrenched. Left unaddressed, the current approach risks weakening Europe’s recycling base and diluting CBAM’s effectiveness as a carbon leakage instrument.

About the contributors:

Alcoa Corporation is active in all aspects of the upstream aluminum industry with bauxite mining, alumina refining, and aluminum smelting and casting. The company has direct and indirect ownership of 25 operating locations across eight countries on five continents, including Spain, Iceland and Norway. Alcoa has an ambition to reach net-zero emissions (Scope 1 and Scope 2) by 2050, with interim targets to achieve a 30% reduction by 2025 and a 50% reduction by 2030.

For more information, contact: Lambert Guilbault, [email protected]

Aluminium Dunkerque specialises in the manufacture of slabs and ingots, in a wide variety of alloys, for high value-added applications in the automotive, transport, and packaging sectors. Major player in primary aluminium in Europe, the plant is based in Loon-Plage, Northern France, since 1991. As one of the world leaders in low-carbon aluminium production, Aluminium Dunkerque has reduced its emissions (scope 1,2) by 17% since 2013 and emits four times less greenhouse gases than the global average for the sector. The company intends to play a major role in the European production of low-carbon aluminium for the benefit of its customers and communities. It is accelerating its energy and environmental transition as part of an ambitious decarbonization project called LowCAl.

For more information, contact: Manon Esperandieu, [email protected]

Constellium is a global sector leader that develops innovative, value-added aluminum products for a broad scope of markets and applications, including aerospace, packaging, and automotive. Constellium generated $8.4 billion in revenue in 2025.

For more information, contact: Catherine Athenes, [email protected]

Norsk Hydro is Europe’s largest aluminium company, operating in 21 European countries and employing over 18,000 people across the continent. The company’s global presence spans more than 40 countries and covers the entire aluminium value chain, from bauxite mining, alumina refining, and aluminium smelting and recycling to the world’s largest network of aluminium extruders. Hydro also produces renewable energy to power the green industrial transition. Its roadmap to achieve net-zero emissions by 2050 or earlier is aligned with the objectives of the EU Green Deal.

For more information, contact: Ana Mingo, [email protected]

Rio Tinto is global leader in aluminium, with a large-scale, vertically-integrated business: bauxite mines and alumina refineries as well as smelters producing aluminium certified as responsible, to now being able to offer fully recycled aluminium products through our Matalco joint venture. Managing the process from start to finish allows us to bring quality products to our customers reliably and efficiently: from high-grade bauxite for the global seaborne trade to sustainably sourced aluminium for beverage packaging to new, lighter alloys for the automotive industry. Our Canadian operations average in the first decile of the industry cost-curve and produce aluminium using clean, renewable hydropower.

https://www.riotinto.com/en/products/aluminium

For more information, contact: Jonathan Vanherberghen: [email protected]

Speira is a leading European aluminium rolling and recycling company, comprising a total of eleven sites in Germany and Norway, as well as its own research and development. Speira recycles up to 650,000 tons of aluminium per year and produces around one million tons of advanced rolled products. Its plants include the Alunorf joint venture, the world’s largest aluminium rolling mill, and Grevenbroich, the world’s largest refining plant. With more than 5,000 employees, Speira supplies some of the best-known industrial companies across the automotive, packaging, printing, engineering, building, and construction sectors.

For more information, contact: Ute Just, [email protected]

Any opinions expressed in this commentary reflect the views of the authors and not of Carbon Pulse.

Carbon Pulse allows subscriber companies to submit one piece of ‘Contributed Content’ (op-eds, advertorials, tenders/RFPs, etc) per year. This post appears in front of our paywall, so it’s readable by anyone. It also appears in our CP Daily newsletter once. Beyond that, or for non-subscribers, we allow companies to purchase ‘Sponsored Posts’. These posts also appear in front of our paywall, while we feature them in our daily newsletter for three consecutive days (instead of one).

You can read more about our Contributed Content/Sponsored Post offering here: https://carbon-pulse.com/advertising-brochure/