By Marcin Laskowski, Vice-President of PKEE – Polish Electricity Association Management Board

The July revision of the EU ETS Directive will determine whether the EU can reconcile it with industrial competitiveness. In short, whether it can achieve decarbonisation without deindustrialisation. Expectations are high – but the stakes are even higher.

Competitive gap between the EU and the rest of the world is growing

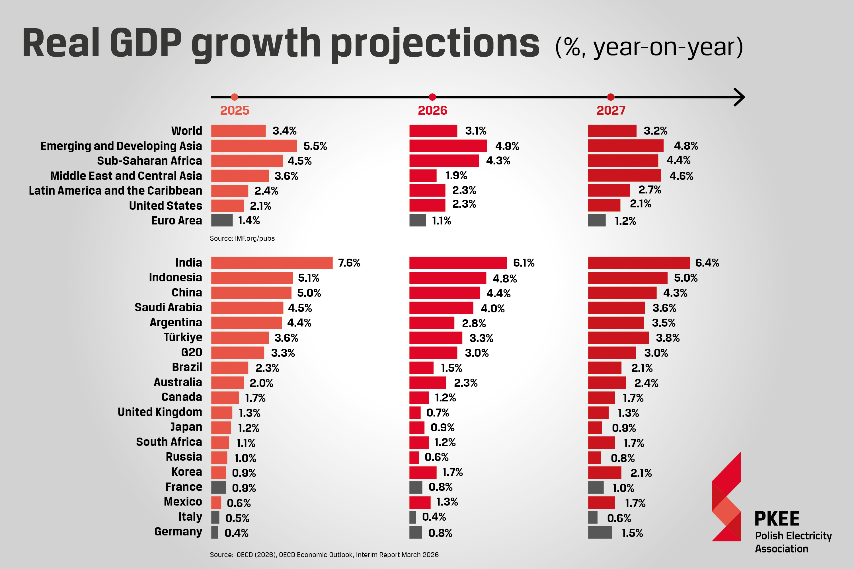

Europe now operates in a very different environment than when many of its climate policies and instruments were originally designed. According to the Organisation for Economic Co-operation and Development (OECD) and International Monetary Fund (IMF) forecasts, EU economies are expected to remain among the slowest-growing in the G20 in the coming years, while the gap between Europe and major competitors such as the US and China continues to widen.

At the same time, European industry faces structurally higher energy costs. This is not a short-term fluctuation, but a trend. The International Energy Agency’s (IEA) Electricity 2026 report underlines the scale of the challenge. EU electricity prices for energy-intensive industries remained elevated in 2025, averaging more than twice US levels and almost 50% above those in China. Wholesale electricity prices followed the same pattern: the EU recorded the highest levels among the markets analysed by the IEA, matching the twofold gap with the US, while standing significantly above levels in India, Australia, and Japan. The report also points to the role of EU ETS prices in maintaining upward pressure on electricity costs.

If European industry pays much more for electricity than its global competitors and, at the same time, bears higher climate-related regulatory costs, policymakers cannot simply take it for granted that companies will remain, invest, create jobs, and decarbonise within the EU.

The EU ETS revision – Time to Rebalance Priorities

A growing number of stakeholders – including industry representatives, energy-intensive sectors and member states facing more challenging transition pathways – are highlighting: the rising cost burden imposed on citizens in the EU. These costs are not abstract. They shape investment decisions, production costs, energy prices, and the ability of European businesses to compete with companies operating in regions where energy is cheaper, regulatory and administrative burdens are lighter, and economic growth is faster. The costs associated with the EU ETS already account, on average, for 11% of industrial electricity prices in the EU. However, in many countries it is substantially more. For instance, in Poland it is around 50% – despite the country having already decommissioned 22 GW of coal-based capacity between 2010 and 2022. This is proving to be an obstacle to accelerate electrification in many member states – which is counterproductive to the EU’s Clean Industrial Deal.

The fact that it is not just about the figures is illustrated by examples such as the latest report from the EU chemical industry (Cefic). It shows that chemical plant closures in Europe have increased sixfold since 2022, reaching 37 million tonnes (Mt) of capacity – around 9% of European production capacity – and leading to the loss of 20,000 direct jobs. The report also points to a sharp slowdown in new investments, with energy cost competitiveness cited as the main reason for closures in 49% of cases, ahead of demand-related factors (19%), overcapacity (9%), and regulation (8%).

This serves as an important reminder that the key question is how to reduce emissions while preserving industrial competitiveness, economic resilience, jobs, energy security, and public acceptance of the EU’s climate agenda across all 27 member states.

“Business as Usual” won’t work

Climate policy is increasingly dividing EU citizens and fuelling euroscepticism. In this context, it is worth referring to the conclusions of the European Council of 19 March, in which heads of state and government called for the EU ETS review to “reduce the volatility of the carbon price and mitigate its impact on electricity prices“. This message was reaffirmed in the June European Council conclusions, which recalled the need to accelerate work on lowering energy prices.

Yet the danger is that the post-2030 climate framework, including the EU ETS review, will repeat the logic of the past, even as the external environment has fundamentally changed. Previous reforms were designed primarily around the internal allocation of costs, benefits, and competitiveness within the EU, with limited consideration for Europe’s position in an increasingly competitive global economy, the strategic importance of energy security, or the growing risk of industrial relocation outside the Union. The EU’s climate policy model, based mainly on cost pressure from CO2 allowances, might be rational in a world where the EU enjoyed a strong economic position and had no serious competitors capable of scaling industrial production cheaper and faster. But that is not the world we live in anymore.

The US combines much lower energy costs with powerful industrial incentives. China combines scale, speed, state support, and control over key clean technology supply chains. Asia and other emerging economies are growing faster and attracting investment.

Therefore, the key to restoring Europe’s industrial competitiveness lies above all in affordable and secure energy. For many industries, this is the foundation of competitiveness. Especially if the EU’s priority is faster and more widespread electrification. EU competitiveness should not be built primarily on imposing high EU ETS costs on European industries. It should be built through incentives, investment support, regulatory simplification, infrastructure development, and access to affordable energy. Europe should reward decarbonisation, but it should not finance one part of the transition by overburdening another part of its industrial base. Moreover, planned, large-scale electrification requires particular attention to the energy sector.

EU ETS reform – solution for all 27 member states needed

Three elements should be at the heart of the upcoming reform.

Addressing the link between carbon costs and power prices would bring down energy costs across the entire EU in a systemic way, which would be far more effective than the current subsidy race. In order to do so, we propose increasing CO2 price predictability by making intervention in the EU ETS market more realistic.

Moreover, a specific volume of energy directed to final customers should be exempted from the obligation to purchase allowances. In exchange, installation operators should reduce their emissions by a specified percentage to comply with the EU 2040 and 2050 climate targets. The volume of energy corresponding to the emission volume should be allocated directly to industrial end-users, at a price that reflects the absence of carbon costs.

Market liquidity needs to be restored. With the current EU ETS parameters, the supply of CO2 allowances on the primary market will end around 2040. The Market Stability Reserve (MSR) will be empty by that time and will not be able to mitigate supply constraints, which will probably occur due to economic recovery after the end of the war in Ukraine, the increase in EU defence capabilities, as well as the insufficient supply of decarbonised gases to replace natural gas.

Therefore, to prevent a market squeeze, the EU ETS revision should, in the first place, substantially reform the MSR parameters. The already presented proposal to abolish the invalidation of allowances by the MSR is the right move, but more needs to be done. The current Total Number of Allowances in Circulation (TNAC) indicator is static and does not reflect the number of allowances held in speculative long-term positions. We suggest introducing a dynamic TNAC to better reflect market circumstances. We also recommend lowering the Linear Reduction Factor (LRF) to reach climate neutrality by 2050, not 2040 as is currently the case. What is more, peaking units, which ensure system stability and adequacy, should be exempted from the obligation to surrender allowances. International carbon credits should also be integrated into the EU ETS.

A focus on affordability and investments is needed. Further decarbonisation of power systems is becoming more challenging, as the remaining emissions are more costly and difficult to abate. The EU ETS auction revenues (estimated at €1.5 trillion by 2050) are expected to cover only 11% of the sector’s total investment needs. Since the whole economy benefits from energy infrastructure, initiatives such as the recently announced €30-billion ETS Investment Booster should support the energy sector. It is also of the utmost importance to maintain the Modernisation Fund in the post-2030 framework, which needs to be continued at the level of 4.5% of the total pool of allowances. Furthermore, the standard and additional allocation of free allowances for district heating should continue after 2030.

Key message

To summarise, our key messages are as follows: the EU ETS must be fit for current and future challenges. It must aim not only at emissions reductions, but also at energy security, price affordability, industrial competitiveness, resilience, and increasing defence production. The EU ETS must be resilient to shocks. At present, it lacks any effective measure to prevent price shocks. The current mechanism to stabilise carbon prices is based on a complex calculation of average price levels over extended periods of time; as a result, it has never been activated, and the current trigger level is around €165. Last but not least, the lack of a comprehensive EU ETS reform will trigger more country-specific measures developed by governments to ease the ETS impact on national economies. This will lead to further fragmentation of the Single Market and would place member states with limited budgetary capabilities at a disadvantage.

The real test of the next EU ETS reform is not whether it drives decarbonisation, but whether it can do so without driving industry away. Decarbonisation has to strengthen the competitiveness of the entire EU, not only selected sectors, companies or member states. It should not be only for first movers, but for the entire European industry. If the transition does not work for all 27 member states – respecting their diverse energy mixes, industrial structures, investment capacities, and regional specificities – the EU’s climate policy risks deepening economic divergence within the Union and deepening the gap between the EU and the rest of the world. What’s more, it will fuel Euroscepticism.

Marcin Laskowski is Vice-President of the Polish Electricity Association (PKEE) and sits on its Management Board.

Any opinions expressed in this commentary reflect the views of the authors and not of Carbon Pulse.

Carbon Pulse allows subscriber companies to submit one piece of ‘Contributed Content’ (op-eds, advertorials, tenders/RFPs, etc) per year. This post appears in front of our paywall, so it’s readable by anyone. It also appears in our CP Daily newsletter once. Beyond that, or for non-subscribers, we allow companies to purchase ‘Sponsored Posts’. These posts also appear in front of our paywall, while we feature them in our daily newsletter for three consecutive days (instead of one).

You can read more about our Contributed Content/Sponsored Post offering here: https://carbon-pulse.com/advertising-brochure/